Who will manage your real estate portfolio when you’re no longer able to?

Families with significant real estate holdings tend to have complex wills and trusts, and transitioning a real estate portfolio after the head of a family passes can be an intricate and stressful process.

“At Whittier Trust, our goal is to help families hold on to their assets, not just sell them,” says Thomas J. Frank, Executive Vice President. “We want to build a relationship, understand your portfolio and intentions for the future, and get plans in place long before succession becomes an issue, while the wealth builder of the family is still alive and running things.”

While many asset managers avoid direct ownership of real estate assets, the Whittier team has decades of experience in a wide variety of property ownership scenarios and structures. “For example,” Frank says, “Sometimes real estate is owned directly in the family trust. By moving the assets into structures like LLCs, we add a layer of liability protection and more easily segregate ownership interests.”

Charles Adams III, Executive Vice President and Manager of Whittier Trust’s Real Estate Department, provides some other examples. “Some families have vacant land,” he says, “and then we have to decide whether that's a long-term hold because it's not creating income. It might be a liability, or it might be a very productive property with a good tenant and strong rental income, but the lease will be expiring soon. Then we’d need to discuss whether the family wants to sell it or retain it depending on the tax situation, cost basis, and the market.”

The Next Best Thing to Family

Whether you hope to have a family member take over the business or you need an unbiased fiduciary partner like Whittier—or both—the time to start making a plan is today. “We work with your attorney and accountant to ensure the properties are owned in flexible yet durable entities,” Frank explains. “We sit beside you as you manage the business so we can understand your style and priorities and be ready to step in if necessary.” Whittier Trust is primed to communicate with beneficiaries, tailoring conversations and reports to each family member's level of involvement and interest. When necessary, the team of advisors oversees property managers, making sure leases are renewed, repairs are made, capital improvements are considered, and new tenants are found.

“You need to have a capable, engaged team in place,” Adams adds. “You need brokers, appraisers, leasing agents, salespeople, and financing people, just to name a few, and Whittier can provide all of those with appropriate oversight. A lot of times, the family patriarch or matriarch has been serving in all these roles themselves. That’s fine, except that it may not provide for succession in the family.”

Adams notes that there are often differing levels of interest from the next generation—some may never have had an interest in the business or the opportunity to learn the business. “That's where Whittier Trust comes in,” he says. “We have a strong network of resources and systems for handling these affairs, no matter how complicated. We offer whatever level of support is needed, from full management oversight to simply serving as backup. As one client recently told me, Whittier is ‘the next best thing’ to family.”

Tailored to Each Family’s Capacity

One example Adams shares is of a family who owned a number of industrial properties. The parents, in their late 80s, had named a daughter to act as successor co-trustee alongside Whittier Trust. But in private, the daughter asked the Whittier team to do all the decision making, saying she would sign off on whatever was recommended. Although that request didn’t align with Whittier’s goals to keep family involved, Adams and his team understood that she was overwhelmed—that she didn't know as much about real estate as her parents might have assumed. So they set up a de facto board that she could be a part of to gradually learn about the business while also having voting rights.

“We’re also happy to work with families that haven’t managed to plan ahead, though of course it’s much more difficult,” Adams says. One client, for example, came to Whittier Trust when the patriarch was already experiencing memory loss. They owned an office building with nearly 50 tenants, but the tenants were no longer getting consistent services because the father didn’t realize he couldn’t manage it by himself anymore. The two adult children relied on the income from this property, but that income was drying up because tenants were leaving or simply not paying rent. So the Whittier team had to go in, sort it out, and get everything running smoothly again.

No matter what the situation, when Whittier Trust serves as a trustee, our role as a fiduciary means we will implement what's in the best interest of all the beneficiaries and the properties without bias. Our deep experience working hand-in-hand with real estate-owning families is a proud distinction of Whittier’s 40-year history as a boutique multi-family office, and our very favorable client-to-advisor ratio is the hallmark of our business. We take pride in our role as stewards of your family’s legacy.

To learn more about how Whittier Trust can make a difference for you and your loved ones, start a conversation with a Whittier Trust advisor today by visiting our contact page.

From Investments to Family Office to Trustee Services and more, we are your single-source solution.

In a recent roundtable discussion hosted by the San Diego Business Journal, Whit Batchelor, Executive Vice President and San Diego Regional Manager at Whittier Trust, joined fellow Southern California wealth management professionals to address the most pressing questions facing clients today.

How do I strategically incorporate philanthropic vehicles like a donor-advised fund or family foundation into my comprehensive wealth management plan and overall asset allocation?

Integrating philanthropy into your wealth management strategy requires thoughtful coordination between your giving goals and tax planning. Private foundations and donor-advised funds offer powerful legacy-building opportunities, but with important distinctions in tax treatment and governance that must inform your selection.

Strategic asset selection can significantly enhance tax efficiency. Non-income producing assets like car collections, vacation properties, or significant artwork often represent ideal philanthropic contributions–potentially providing substantial deductions while converting non-cash-flowing assets into charitable impact. We approach this holistically, viewing your wealth across three dimensions: assets inside your estate, outside your estate, and within philanthropic entities.

This integrated perspective allows us to optimize your philanthropic impact while creating meaningful tax advantages and preserving family values across generations.

I’m considering splitting my time between California and other locations. What strategic tax planning approaches should I implement to legitimately minimize my California income tax exposure?

California residents approaching business transitions or retirement often have unique opportunities to optimize their tax situation while fulfilling lifestyle goals. Strategic planning around residency can yield significant tax advantages–particularly when spending time in non-income tax states like Nevada, Washington, Texas, and Florida.

Proactively establishing non-California trusts or entities prior to significant liquidity events can dramatically reduce tax exposure when selling business interests. Similarly, establishing legitimate residency in no-income-tax states before drawing on retirement accounts can preserve substantial wealth.

We emphasize that “asset location” is as critical as asset allocation in comprehensive wealth planning. This includes thoughtful positioning of assets across various jurisdictions to leverage beneficial tax treatment both inside and outside high-tax states like California–creating long-term advantages while supporting your desired lifestyle.

I’ve built a substantial portfolio of investment real estate that has appreciated significantly, creating potential estate tax exposure. What sophisticated strategies would you recommend for transferring these properties to my children in a tax-efficient manner?

California’s remarkable real estate appreciation over recent decades has created both opportunity and challenge–with many families holding properties now exceeding lifetime estate tax exemptions. The goal becomes transferring these high-value assets to future generations while addressing several competing concerns.

Effective strategies must balance estate tax minimization with maintaining control and preserving cash flow during your lifetime, while also considering California’s property tax implications. Tools like Spousal Limited Access Trusts (SLATs), intentionally defective grantor trusts, and qualified personal residence trusts can be particularly effective.

Strategic discounting through family limited partnerships or LLCs can further enhance transfer efficiency. These sophisticated approaches allow significant real estate value to move outside your taxable estate while retaining income streams and influence–preserving both wealth and your desired lifestyle during retirement.

Our family’s wealth has grown substantially in both value and complexity. What solutions should we consider for streamlining this complexity and ensuring seamless continuity if either of us becomes incapacitated or passes away?

As family wealth grows in complexity, what was once intellectually stimulating can eventually become burdensome–especially as priorities shift toward lifestyle enjoyment rather than wealth management. This challenge becomes particularly acute when responsibility has primarily rested with one spouse, potentially creating significant stress for a surviving partner.

Multi-family offices provide an elegant solution by offering comprehensive services that address both investment management and administrative complexity. Services like bill payment, household accounting, bookkeeping, tax coordination, and compliance management create a seamless infrastructure that functions reliably regardless of family circumstances.

This integrated approach ensures continuity during difficult transitions and provides peace of mind that your affairs will be managed according to your wishes–protecting both your surviving spouse and future generations from administrative burdens that they may be unprepared or unwilling to shoulder.

Answers provided by Whit Batchelor, Executive Vice President and San Diego Regional Manager with Whittier Trust.

If you have more questions about philanthropic planning, real estate strategies, tax-efficient wealth transfers, or simplifying complex family finances, start a conversation with a Whittier Trust advisor today by visiting our contact page.

From Investments to Family Office to Trustee Services and more, we are your single-source solution.

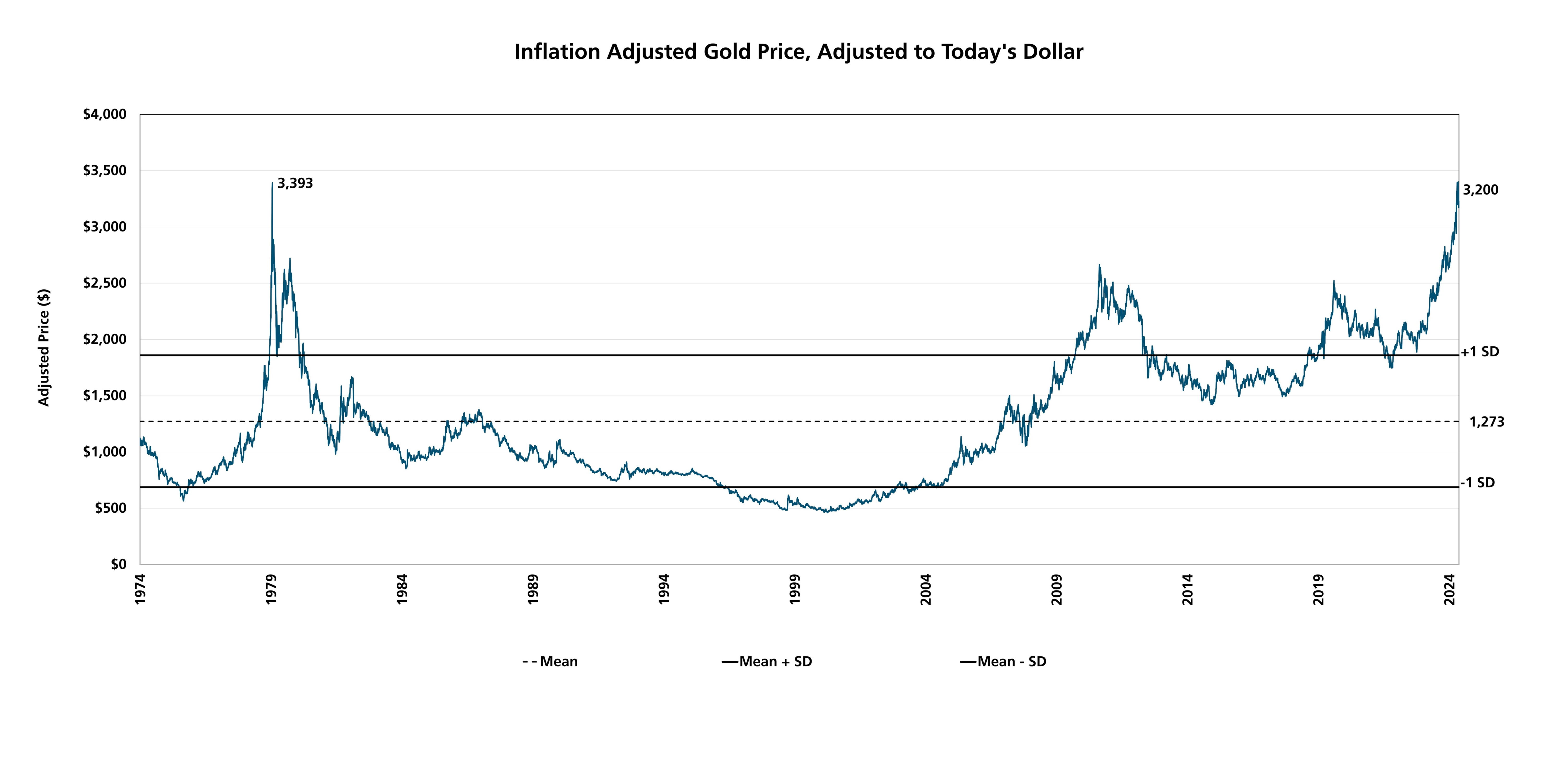

In investing, “value” is a word that’s used often but rarely understood in depth. It is not just a price tag, an item on a balance sheet, or a line on a chart. Rather, value is a complex blend of trust, expectation, and the interplay between certainty and speculation. The recent surge in gold prices to record highs—driven by central banks seeking safe havens and investors responding to global uncertainty—has reignited a timeless question: What is something truly worth?

As a result, we’re sharing more about the logic of value across asset classes, moving from the most predictable to the most speculative, and revealing how different forms of value are calculated, perceived, and ultimately believed.

Bonds: The Arithmetic of Certainty

Bonds are the bedrock of financial predictability. These instruments are essentially contracts: You lend money, receive regular interest, and—assuming no default—get your principal back at maturity. Their valuation is rooted in arithmetic:

Present Value of Future Cash Flows: Each coupon payment and the return of principal are discounted to today’s value using prevailing interest rates.

Yield to Maturity (YTM): This is the expected rate of return if the bond is held to maturity.

Credit Spreads: Non-government bonds require higher yields to compensate for additional credit risk.

While factors like inflation, interest rate changes, and shifts in creditworthiness add complexity, bonds remain anchored in accountability and well-defined terms. They represent the closest thing to certainty in the investment world.

Real Estate: Tangible and Local

Real estate offers visibility and utility. Properties can provide income through rent and often appreciate over time. Valuation in real estate relies on several methods:

Comparable Sales (Comps): What have similar properties sold for in the area?

Income Approach (Cap Rate): Calculated as Net Operating Income divided by Property Value, this method is key for income-producing properties.

Replacement Cost:What would it cost to rebuild the property today?

Real estate is about more than numbers; it’s about neighborhoods, tenants, and local narratives. While the fundamentals are solid, they are never static. Location can create value, while a poor tenant can erode it. The reverse is also true. The asset’s tangibility and the potential for steady cash flows make real estate a unique blend of predictability and variability.

Stocks: Ownership with Imagination

Owning a stock means holding a claim on a company’s future earnings, decisions, and relevance. Unlike bonds or real estate, stocks are inherently forward-looking and subject to interpretation. Key valuation methods include:

Discounted Cash Flow (DCF): Projecting a company’s future cash flows and discounting them to present value based on risk and time horizon.

Sum of the Parts (SOTP): Valuing each underlying business or asset separately to determine the overall worth.

Earnings Multiples and Dividend Models: Using metrics like price-to-earnings ratios or dividend discount models to gauge value.

Stock prices swing on earnings reports, macroeconomic shifts, and geopolitical events. Yet, in the long run, fundamentals—such as earnings growth—tend to prevail. Successful investors are those who can distinguish signal from noise and think in years rather than days.

Gold and Precious Metals: The Value of Belief

Gold sits at the far end of the valuation spectrum. It generates no income and pays no dividends, yet it endures as a store of wealth. Its value is driven by:

Scarcity: Mining is slow and costly, and supply is limited by nature.

Macroeconomic Trends: Inflation, currency debasement, and global uncertainty boost demand.

Market Psychology:In times of turmoil, investors seek gold for safety, not returns.

Recent years have seen gold prices soar to historic highs, with forecasts for 2025 ranging from $3,000 to nearly $3,700 per ounce as central banks and investors seek protection from economic and geopolitical risks. Unlike other assets, gold’s value is almost entirely a matter of belief—that is, confidence that others will continue to see it as a safe haven when other systems falter. In this sense, gold is as much about philosophy as it is about finance.

Value, Reconsidered

Tracing the arc from bonds to gold is a journey from definition to interpretation—from contractual returns to collective belief. Each step reveals not just how we price assets, but how we understand risk, reward, and resilience.

Warren Buffett famously said, “Price is what you pay. Value is what you get.” But what you get depends on how well you understand what lies beneath the numbers. In a world obsessed with immediacy, the ability to think in fundamentals-across asset classes and through market cycles-is a quiet but powerful advantage.

Ultimately, value is not just a calculation. It is a reflection of human judgment, emotion, and conviction—qualities that no formula can fully capture. At Whittier Trust, we understand value, both in the mechanics of strategically selecting assets that make sense based on our clients’ present needs and future legacy goals, but we also make it our business to understand each client’s underlying concerns.

Written by Caleb Silsby, Executive Vice President, Chief Portfolio Officer at Whittier Trust. Caleb oversees a team that collaboratively manages portfolios for high-net-worth clients, foundations, and endowments. He is credentialed as a CFA Charterholder and CFP professional.

If you’re ready to explore how Whittier Trust’s tailored investment strategies can work for you, start a conversation with a Whittier Trust advisor today by visiting our contact page.

From Investments to Family Office to Trustee Services and more, we are your single-source solution.

Investing is a balancing act between risk and reward in the best of times, but today’s uncertain economic climate and fluctuating markets present an unprecedented challenge for investors. While some people choose to stay with traditional options like money market funds and government bonds, others are taking on more risk with hard-money lending and alternative investments – everything from cryptocurrency to classic cars.

“Given the volatility in the equity markets, some investors are reducing risk in their portfolios due to a slowing economy, stubborn inflation, and uncertainty around trade policies,” said Dean Byrne, regional manager of The Whittier Trust Company of Nevada, which has offices in Reno, Portland, Seattle, and Austin, Texas. Byrne said the U.S. is currently in a “risk-off” environment, in which investors are more risk-averse and are selling assets like stock and moving their money to lower-risk options. As a trust management company, Whittier Trust offers a wide range of financial services. Its investment management team handles core assets, such as equities, fixed income and real estate.

In general, Nevada follows national trends in investing, such as increasing interest in digital assets like cryptocurrency, which have become widely accepted, even by institutional investors and hedge funds. Technology is also driving increased interest in companies that supply the energy needs and the physical infrastructure (think data centers) for the growing artificial intelligence (AI) sector. “We see an enormous amount of capital being deployed into public and private AI investments on the expectation of continued growth and attractive returns,” said Byrne.

The migration of wealthy Californians to Nevada is changing the nature of investing in the Silver State, according to Nevada Secretary of State Francisco Aguilar, whose office performs registration and oversight of securities, securities brokers and dealers, and investment advisors. “Enclaves like the Summit Club in Summerlin bring the investor-minded type of individual to Nevada, and with that comes more opportunity to invest in private placement deals, real estate offerings, private credit offerings, cryptocurrency, gold and silver,” he said. “[These new residents] are sophisticated investors who are looking to diversify their portfolios. There’s more investing in Nevada now than in previous years because these people bring their money and their investment portfolios with them.”

One option for savvy investors looking for diversification is hard money lending. “We specialize in private lending, with multiple lenders joining together to fund loans on Nevada real estate,” explained John Blackmon, owner/broker of NV Capital Corporation, a private lending and investment brokerage based in southern Nevada. “Our property-backed hard money loans make financing available on a wide variety of single-family and multi-family homes, business buildings, and land for development. Many people choose a trust deed investment because they are looking for more secure, high-yield returns. If properly structured by a specialized broker, trust deed investments have the potential to yield favorable returns – especially when you look at other investment options with similar risk profiles. That’s because your risks are mitigated by the value of the property being used as collateral against the loan.”

People who don’t mind taking some additional risk may consider any one of a number of alternative investments. “Alternative investments are a broad asset class, but narrow down to investments outside of traditional cash, bonds and stocks,” said Byrne. “Real estate, cryptocurrencies, blockchain, private equity, hedge funds, commodities, even collectibles like art, coins and classic cars, fall into the alternative investment bucket.”

Byrne pointed out that owning a business could also be considered a form of alternative investment, with its own level of risk and reward. “Business owners usually reinvest all their profits into their own company,” he said. “In essence, they’re investing in one stock, and they’re comfortable with that risk. Yes, it may keep them up at night sometimes, but they know it inside and out, and it’s familiar.”

He added that Nevada provides a better opportunity for multi-generational wealth creation than other states because it doesn’t have an estate tax and it offers favorable laws allowing a business owner to transfer business interests into a trust. “Gifting interests in a family business to the next generation is a powerful tool, and if structured appropriately, allows for succession planning, building and protecting family wealth, avoiding probate, and reducing taxes,” he said.

What Should New Investors Know?

“What I tell my children and grandchildren is that they can still get about 4 percent in a US Treasury mutual fund,” said Blackmon. “That’s a good place to be right now. It’s fairly risk-free, and at least your money is making something. Be a little disciplined and every so often move some money from a regular bank account to a money market fund to get some interest. Then, if you have some money to invest and don’t mind a little risk, you can get into a small deal with a trust deed. One of my kids did that and they enjoy driving out and looking at their collateral.”

Byrne recommended that new investors start with a clear goal. “What are you trying to accomplish? Are you investing for retirement, a large future purchase, building wealth or simply creating a shoot-for-the-moon portfolio – one with high risk and potentially high reward? If that investment goes to zero, you have to be okay with that. Higher risk should come with a higher return, but it doesn’t always work as planned. Most people want investments that enable them to sleep at night.”

He advised new investors to think long-term and be prepared to weather the short-term ups and downs of the market. “It’s important to remember the adage: ‘Time in the market is better than timing the market,’” he said. “In the first week of April, [the stock market] had some pretty rough days. Then, with the announcement that tariffs were being delayed for 90 days, the S & P jumped seven percent, just like that. Nobody could have predicted that amount of volatility or timed it appropriately. Just start early and invest consistently, in good times and bad times. Long-term investments lead to appreciation and compound interest.”

Aguilar would advise a new investor to perform their due diligence before trusting anyone with their money. “Research who will be managing your money and guiding your investments,” he said. “Call the Secretary of State’s office to verify that they’ve been licensed. Doing the verification process will save you a lot of heartache. If the investment vehicle is complicated, get someone to explain it to you in terms you can understand, and trust your gut. If it sounds too good to be true, it isn’t [true].”

Avoiding Fraud in a Dangerous World

While there is a certain amount of risk in any investment, a very real risk is becoming a victim of a fraudulent investment scheme. Aguilar reported that in fiscal year 2023, his Securities Division received complaints of securities fraud from investors totaling more than $16 million, and in fiscal year 2024 that number was almost $10 million. Fraud cases are investigated by the Securities Division and prosecuted by the state attorney general and county district attorneys.

“We’re especially looking out for what’s called ‘pig butchering,’ which typically targets males with a social media presence,” Aguilar said. In this scheme, scammers build relationships with victims through social engineering to lure them into investing in fake opportunities or platforms, ultimately leading to financial losses. They “fatten the pig before slaughter” by getting them to make increasing monetary contributions, generally in the form of cryptocurrency, to a seemingly sound investment before the scammer disappears with the contributed monies.

“When that happens, people are often embarrassed to tell us that they’ve been the victim of investment fraud,” said Aguilar. “In addition, many of the fraudsters are located overseas and it’s hard to get jurisdiction over these individuals. What we can do is make sure the marketplace is educated about these issues so they don’t fall victim to them.” He advised investors to make sure they are dealing with a licensed advisor or a broker-dealer with a good reputation – someone who’s a part of the industry, not just a random person who contacted them online.

“Find a reputable financial advisor to guide you,” said Byrne. “Read the fine print about their fee structure and any proposed investments. Don’t be afraid of getting a second opinion.”

Blackmon advised people considering hard-money lending to ask to see an appraisal or a broker price opinion on the property. “That will give you a third-party valuation that the property is worth more than the proposed loan amount,” he said. “Be sure to go with a company with experience in real estate lending, and in my opinion, you should go with a brokerage company that uses a third-party service to collect the monthly payments from the borrowers and distributes them to the investors. Unscrupulous brokers may otherwise divert the payments to their own account and be tempted to use that money for other purposes. It’s just one more level of protection.”

Aguilar noted that, although reported losses to fraudsters total millions of dollars each year, victims of fraud often lose their entire life savings and are not compensated. Many guilty parties in securities cases do not have any money to pay court-ordered restitution to their victims. In FY 2023, investors received restitution of only $205,000 and in FY 2024 it was just over $1 million. His office is supporting a bill in the Nevada Legislature this year that aims to fill the gap between the restitution that’s owed to victims and what they actually receive. Senate Bill 76, entitled “Victim Restitution Act,” would create a fund from monies received from enforcement actions due to violations of the Nevada Securities Act (NRS 90). Nevada residents who have received an award for restitution in a criminal conviction can apply for restitution from the fund if they don’t get repaid from the fraudster.

“The main reason we are proposing this legislation is that it provides a way for Nevada residents to obtain desperately needed relief after losing what is often a significant chunk of their savings to someone who has defrauded them,” said Aguilar. “Often, victims of securities fraud are in the most vulnerable communities, especially our senior communities and others on fixed incomes.”

"Safe" is Relative

Aguilar advised potential investors to discuss the level of risk with their money manager and decide what they’re comfortable with. “100 percent safe would be putting cash in your mattress, but even then, you run the risk of theft,” he said. “Putting your money in an FDIC-insured checking or savings account is safe, but there’s the opportunity cost of giving up a chance for appreciation, and inflation may erode the value of your principal. Medium-risk may be S&P 500 stocks, and high-risk would be private-party deals or hard money investments. You should only take high risks if you have the capacity, and if it won’t change your lifestyle if you lose your investment.”

“Safe is a relative term,” agreed Byrne. “Cash in a low-yielding, FDIC-insured bank account has risks of eroding your purchasing power due to the effects of inflation.”

What's Ahead?

“Right now, we have a fairly new president and there are some unknowns about tax policy and other things,” said Blackmon. “We’re not sure if that will lead to more investments in real estate or to fewer people willing to invest. This spring, things have slowed down for us because of uncertainty on the macro level. If you’re thinking of building an $83 million building, you’d be a little nervous to start. You may want to wait a few months before investing, to see which way the wind is blowing and what interest rates will be doing. Some people say tariffs won’t cause interest rates to rise, but it seems to me that increasing costs will lead to an increase in interest rates. I’m looking forward to being proved wrong. It will be interesting to watch what’s ahead in the next six months. I still look to the US government, even with whatever issues are going on right now. It’s the best country in the world.”

Featured in Nevada Business Magazine. For more information on Whittier Trust's investment services and portfolio management strategies, start a conversation with a Whittier Trust advisor today by visiting our contact page.

From Investments to Family Office to Trustee Services and more, we are your single-source solution.

What ultra-high-net-worth individuals need to consider when mulling an exit.

In my role at Whittier Trust, I've seen firsthand how critical it is for ultra-high-net-worth individuals (UHNWIs) to have a well-thought-out exit strategy for their family businesses. Despite the intensive planning that typically goes into wealth management, recent research from the Exit Planning Institute suggests that a staggering 80% of business owners lack solid exit strategies, leaving their wealth in limbo and risking economic continuity for future generations.

The planning process of an exit strategy can often be fraught with uncertainty and potential pitfalls, making it a critical issue for business owners nearing retirement or a transfer of ownership or leadership. Here are the five key questions UHNWIs should ask their advisors to ensure a smooth and successful transition.

1.How many different exit strategies are available to me?

Understanding the various ways you can exit is fundamental to choosing the right path for your business. Each exit strategy has unique implications and suitability depending on your business's circumstances and your personal objectives. Here's a breakdown:

Generational Family Transfer

When multiple generations of a family are actively involved in the business, an owner might prioritize business legacy and family engagement over the sale price. If the objective is to keep the business in the family, the exit plan might involve transferring company stock, often at a discount, to direct heirs over many years. While keeping a majority stake in the company and control over operations, the owner can transfer assets to the next generation while still mentoring and training the next leader.

A generational family transfer can play out in a variety of ways: the owner may ultimately sell stock in the company to family, retire holding minority ownership or gift all stock to heirs. A successful transfer will take at least three to five years to accomplish, position the business for success, meet the owner's liquidity and financial needs after the transfer and leave the new owner(s) financially stable after the transaction.

Management Buyout

An owner who wants to sell all or part of the company to existing management might favor a management buyout. This type of ownership transition involves structuring a deal in which management uses the assets of the business to finance a significant portion of the purchase price. This can work for an owner who believes in the management team and thinks it will be able to keep the business thriving when he/she exits. However, if the management team lacks adequate liquidity, the seller may have to accept a lower price or unattractive deal terms, including heavy seller financing.

Sell to Partners

When the owner has partners and a quality buy-sell agreement, a sale to partners may be the only selling option. A buy-sell agreement generally articulates a controlled process for transferring ownership. Since the buyers fully understand the business and it's a planned process, selling to partners generally isn't too expensive. Common challenges in selling a business to partners include a lower sale price, slow transfer of proceeds and potential disagreements among partners.

Sell to Employees (ESOP)

When an owner wants to sell the company to its employees, an employee stock ownership plan (ESOP) might be the answer. In this type of sale, the company uses borrowed funds to acquire shares from the owner and contributes the shares to a trust on behalf of the employees. ESOPs require a securities registration exemption and are classified as an employee benefit, so it's an involved process. An ESOP sale takes many years to complete and is generally more expensive and complicated than other options. However, it can be a way to reward valued employees with company ownership. The tax savings to the seller can be substantial as well.

Sell to a Third Party

When the business is healthy and the owner wants to cash out, selling to a third party could be a good option. Whether the interested party is a strategic buyer, a financial buyer or a private equity group, the owner should expect to pay some big up-front costs to engage experienced professionals to guide the owner and company through the selling process. Having the right partners attending to the owner's interests, negotiating with the buyer and structuring deal terms are crucial to achieving the best outcomes.

Although the payoff can be attractive, third-party sales are not for the faint of heart. The process takes at least nine to twelve months and can be intense and emotional for the seller. Often, the seller retains some obligation to the business beyond the sale but has to be ready to give up control entirely. A third-party sale is ideal for an owner who is open to having the buyer bring new energy, ideas and change to the business.

Recapitalization

An owner who is open to having outside investors fund the company's balance sheet might consider bringing in a lender or equity investor to act as a partner in the business. By selling a minority or majority position, the owner can partially exit, monetize a portion of the business and reduce ownership risk in the company. New growth capital can bring more earnings to the original owner. When ready to exit the company completely, the original owner might sell the remaining shares through further recapitalization or another exit option.

Selling any portion of the company to an outsider can precipitate a loss of control and a cultural shift within the company. An owner who is not ready to be accountable to partners should consider this before opting to recapitalize.

2. How long before retirement should I begin thinking about my exit?

Ideally, business owners should start thinking about their exit strategy at least five to ten years before their intended retirement. This period allows for comprehensive planning that can influence key outcomes of the eventual sale. Value-building initiatives need time to succeed and show results before they can impact sale proceeds (valuation optimization). Identifying and grooming a successor — whether a family member, a key employee or an external buyer — is generally most effective over an extended period (succession planning). Structuring the business and the sale to maximize tax efficiency and comply with legal requirements is an involved process (legal and tax planning). Finally, strengthening the business's operations and financial health can make it more attractive to potential buyers (operational improvements).

3. Whatsteps should I take to optimize valuation and transition?

Optimizing your business's valuation and ensuring a smooth transition involves several strategic steps. First, conduct regular financial audits to present clear and accurate financial statements; transparency is key to attracting serious buyers and securing a favorable sale price. Next, take a look at opportunities to enhance operational efficiency to demonstrate the business's profitability and growth potential. This might involve adopting new technologies, improving processes or cutting unnecessary costs. Another crucial step is to develop a strong management team that can operate independently, as a business that doesn't rely solely on the owner is more attractive to buyers. Solidifying relationships with key customers and suppliers is also important, since long-term contracts and stable relationships add value and stability to the business. Finally, ensure the business complies with all legal and regulatory requirements. Any outstanding legal issues can deter buyers or lower the sale price.

4. What if a big part of my exit is going to be a sale or a partial sale?

If you are leaning toward a sale, either partial or complete, several considerations come into play. Engaging professionals is one of the first and most crucial steps. Working with experienced legal, financial and business advisors helps owners navigate the complexities of the sale process. Those professionals can also help with due diligence. Buyers will conduct thorough examinations of every facet of your business, including financial records, legal documents and operational data. Being prepared with detailed and organized documentation can facilitate a smoother due diligence process and instill confidence in potential buyers. This preparation not only expedites the sale process but also helps in presenting your business as a well-managed and transparent entity, which can lead to a more favorable sale price.

Identifying potential buyers is also a strategic consideration that can greatly influence the sale’s success. Depending on your business's nature and industry, potential buyers could be competitors, private equity firms or even international investors. Identifying and approaching the right buyers ensures that you attract parties who see the most value in your business.

5. How should I structure sale deals?

Structuring a sale deal requires careful planning and negotiation to balance your needs with the buyer's. This involves key elements like payment terms, which can be a one-time lump sum or installments. You might even consider seller financing, which can make the deal more attractive but comes with the risk of the buyer defaulting. Another option is to structure earn-out payments tied to the business’s future performance, which can bridge valuation gaps but require clear metrics and timelines. Noncompete agreements are often requested by buyers to prevent owners from starting a competing business post-sale, so ensure the terms are reasonable and don’t unduly restrict future options.

The structure of the deal can also significantly impact your tax liabilities. Understanding the tax implications of different payment structures is crucial, as installment payments may help spread the tax liability over several years. Work with wealth management advisors to explore strategies that could mitigate your tax burden. Experienced legal counsel can help you draft and review all agreements, focusing on representations and warranties to minimize future liabilities and ensuring provisions for indemnification to protect against potential future claims or disputes.

You will also have to decide whether you'll stay involved in the business after the sale, in either a consulting capacity or a more formal role. This can ease the transition and provide additional income, but it might also limit your ability to fully step away. Don't forget to consider how the sale aligns with your personal and family goals. Reflect on how the sale proceeds will be integrated into your overall estate plan, ensuring the structure supports your legacy and philanthropic goals. Also assess how the sale structure impacts your lifestyle and plans, whether it involves retirement, new business ventures or other personal endeavors.

The transition of a family business is a complex process that requires careful planning and execution. By asking your advisors the right questions, you can ensure a smooth and successful exit that secures your legacy and financial future.

Written by Elizabeth Anderson, Vice President at Whittier Trust. Elizabeth is based out of the Pasadena office and focuses on family business transitions, succession planning and pre-liquidity personal planning.

For more information, start a conversation with a Whittier Trust advisor today by visiting our contact page.

From Investments to Family Office to Trustee Services and more, we are your single-source solution.

Next-gen philanthropy is about more than just giving money away.

Philanthropy is about helping others and offering invaluable funding to support communities and causes. With a family foundation, it’s also about preserving a legacy andbringing family members together in the name of a shared cause or purpose. The styleand look of a family foundation varies, and it’s important to consider how to engage the next generation in all aspects of the foundation.

Junior boards—also called associate boards—can be a powerful tool in helping prime thenext generation for leadership, and they can be highly personalized in structure, style, andpurpose. They can be as small as a few members, or as large as 20 or more, and the agelimitations can be anywhere from pre-teen to mid-30s. These launch pads areinstrumental in not only growing the foundation’s reach but also growing the junior board members as individuals.

“Junior boards help teach the next generation about the foundation and its mission, howit’s structured and more. It’s a good way to strengthen members’ financial literacy skills. Ithelps them learn about the value of money, investing the foundation’s assets, learningabout the stock market and the power of giving with an eye on both strategy and passion,”says Jesse Ostroff, Assistant Vice President and Client Advisor for Whittier Trust’sPhilanthropic Services. Junior boards can also help strengthen familial ties, preparemembers to transition to the main board and help members discover more about themselves. Here’s how.

Strengthening Family Bonds

Junior boards can help strengthen a family’s bond, especially if there are many branchesor if the members aren’t particularly physically or emotionally close. “It’s a good way forcousins or more distant relatives to be able to collaborate and decide how and where themoney should go,” says Ostroff, who adds that working together is helpful in makingjunior board members feel less alone in their giving.

Even close-knit junior boards can deepen their relationship. Ostroff recalls one example of a small junior board that had been working together for many years. Whittier Trustfacilitated an opportunity for them to share during a family retreat, where each membermade a presentation on their chosen grantee organization, describing why they felt it wasworthy of support and providing an overview of the diligence they had conducted on it.“It was during the pandemic so it took place over Zoom,” Ostroff noted, “but it workedreally well, and the subject matter helped them develop deeper connections with eachother and with the foundation Board.” One of the unanticipated outcomes was a numberof cousins deciding to collaborate and support each other’s chosen organizations. “Eventhough you’re family, you don’t always take the time to listen and hear about each other’s interests,” he says. “This opportunity strengthened family ties in a natural, organic way.”

Facilitating Family Continuity

Family foundations often struggle with succession plans, so establishing a well-functioningjunior board can help smooth younger family members’ transition to the main board. Butit also takes intentionality. “Part of our role is to get the junior board excited enough towant to devote time and attention to their philanthropy, despite the competing demands ofcareer and family,” says Ostroff, whose team does this by showing interest in juniormembers as individuals, having strategic conversations with them about the change they’dlike to see in the world, and accompanying them on site visits to grantee organizations sothey can see first-hand the impact they’re having.

Conversely, some junior board members are exuberant and need help focusing their interests and reining their strategies. Ostroff recalls one junior board of teenagers whowere excited to be participating in their family’s philanthropy, but they hadn’t yetidentified a mission and felt daunted by the responsibility to give money away. To theircredit, they wanted to do it right and didn’t know where to begin. “We convened thegroup and used a core values game to help them to identify first the family’s core values,and then their individual values,” he says. “From there, it was easier for them to select oneor two focus areas for their grantmaking, and then to drill down and choose particular nonprofits they wanted to support.”

Inspiring Personal Growth

Ostroff’s favorite aspect of his job is watching junior board members grow through theirparticipation in the family’s philanthropy. “They develop life skills, such as financialliteracy, respectful communication, critical thinking, and collaboration, that set them up forsuccess in their careers and relationships.” As they begin to see the myriad benefits ofaligning their family’s wealth and values, younger family members become more effectivestewards of the wealth they may eventually inherit.

Whittier Trust helps create, manage and develop junior boards, tailoring their recommendations and plans to a family’s philanthropic mission and grantmaking style,while simultaneously helping them find their own philanthropic voice. “As the nextgeneration moves up, there will be new societal challenges, new philanthropic trends andopportunities. Millennial and Gen Z family members are coming of age in a world that iscompletely different from the one their grandparents inhabited,” says Ostroff. “And we’reable to provide them with the tools and support they will need to meet their moment andmake their own impact.”

If you’re ready to explore how Whittier Trust’s tailored philanthropic services can work for you, start a conversation with a Whittier Trust advisor today by visiting our contact page.

From Investments to Family Office to Trustee Services and more, we are your single-source solution.

How smart entrepreneurs future-proof their legacy.

Most entrepreneurs who have built a corporation to a valuation in the hundreds of millions (or higher) will tell you about a beginning filled with hard work, sleepless nights and worry over whether or not their business would survive. We work with many family businesses that are now worth over a billion dollars, but they all started somewhere.

Those early days are the ideal time to strategize for future success by shielding yourself and your business from unnecessary tax burdens, maximizing the impact of your legacy and creating terms that fulfill your vision. However, many of those same entrepreneurs who are so good at building a business from the ground up fail to forecast 20 or 30 years into the future. They're too focused on the now. Unfortunately, by the time a business reaches the pinnacle of its success, it may be too late to fully take advantage of the opportunities that existed early on.

That's where an experienced multifamily office comes in: they are specialists in helping individuals, entrepreneurs and families think far ahead and lay the necessary groundwork for a best-case scenario. The goal is to maximize potential returns and help “future-proof” clients' legacies, allowing them to fully enjoy the fruits of their hard work.

Easing Tax Burdens

When a company isn't worth a fortune, it's easy to forget about what might happen when its value rises. One important step is to qualify for Qualified Small Business Stock (QSBS) when the business is worth less than $50 million. Setting up a business to qualify for the QSBS isn't overly challenging. The entity must be a domestic C Corp, at least 80% of the corporation's assets must be used to conduct one or more qualified trades and originally acquired stock must be held for a minimum of five years, among other requirements. However, this process must be diligently undertaken to ensure entrepreneurs can reap the benefits down the line.

With QSBS, 100% of the gain from a sale can be excluded from federal income tax (subject to certain limitations), which can amount to a fortune if a company is sold for a high value. A number of multifamily office — and, more specifically, those with robust trust services — can both serve in an advisory capacity and handle the execution of the necessary steps (such as engaging and managing the right tax and legal professionals), allowing the entrepreneur to focus on growing the business.

Location, Location, Location

If there's any flexibility regarding where a business is located, multifamily offices can help set owners up in the most tax-advantaged position. For example, businesses located in California are subject to one of the highest corporate tax rates in the nation at 8.84%. If the income is generated by California real estate or headquartered in California, there's no way to escape that rate.

However, if the business can be headquartered in a more tax-advantaged state such as Nevada, which does not levy a corporate income tax, it might be worth considering. To help smooth the generational transition, some families utilize a trust situs in Nevada to hold their shares of the business. Nevada situs can help avoid California income taxes and California capital gains taxes (which amount to 13.3%) upon the sale of the business.

Mitigating Future Estate Taxes

If businesses grow inside a taxable estate, the government takes 40% of the value upon the owner's passing. For entrepreneurs who are building a successful corporation, it can be beneficial to allocate some shares into a trust outside of the taxable estate, where they can grow in value without being subject to the estate tax. There are a variety of trusts that allow owners to reap the benefits of the assets during their lifetimes, while shielding the estate from an onerous tax burden.

Preserving Family Harmony

Finally, it may not be obvious, but it's important to coordinate the estate plans of all family members who are involved in the business to ensure that they are aligned with the overall succession plan. The goal is to put a master plan in place that balances financial, corporate and relational goals so that the business — and the family attached to it — will thrive in perpetuity.

Start Early for Maximum Benefits

If you're reading this and your business isn't (yet) close to the multimillion-dollar threshold, it's still important to take the time to be thoughtful about how you'll set it up for future success. You may be spending your days working on improving the current bottom line, managing staff and investing in refining your product and service offerings. Still, we've seen companies quickly catapult from a few million in assets to a much higher value, so it's important not to wait. Having a go-to team of advisors who can provide both strategy and execution to file necessary paperwork, think critically about the company's financial trajectory and maximize the benefits as it grows.

Written by Brian Bissell, Senior Vice President, Client Advisor in the Orange County office of Whittier Trust.

Featured in Family Business Magazine. To learn more about how Whittier Trust can support you, your family and your legacy through our family office services, start a conversation with a Whittier Trust advisor today by visiting our contact page.

From Investments to Family Office to Trustee Services and more, we are your single-source solution.

Whit Batchelor, from Whittier Trust's Newport Beach Office, is set to lead the expansion, strengthening client and community bonds within the region.

Whittier Trust is excited to announce the opening of its newest office in San Diego, reinforcing its deep commitment to serving clients in the region with a local, personalized approach. With a legacy rooted in Southern California, Whittier Trust has long advised clients and worked closely with charitable organizations based in San Diego. This expansion is a direct result of the wealth management company's continued growth in the region.

"Our decision to establish a full-time presence in the San Diego area reflects both the incredible growth we've seen here and the deep trust San Diego's most successful families have placed in us for decades," said David Dahl, President and CEO of Whittier Trust. "Our expansion into San Diego is also a reflection of our long-standing ties to the community," said David Dahl. "The Whittier family has a deep history in the region, and we are proud to strengthen our presence here, not just to better serve our clients, but to be closer to the charitable organizations and causes we have supported for years."

Whittier Trust's commitment to San Diego extends beyond wealth management, as the firm actively supports a variety of local organizations integral to the community. This includes the Helen Woodward Animal Center, which promotes animal welfare and pet adoption services; Scripps' Mericos Eye Institute and Whittier Diabetes Institute, advancing medical research and patient care; the San Diego-Imperial Council of the Boy Scouts of America, fostering leadership and service among youth; and the University of San Diego, where Whittier Trust contributes to higher education and leadership development initiatives.

Leading the new San Diego office is Whit Batchelor, newly appointed Executive Vice President, Client Advisor and San Diego Regional Manager. A longtime leader in Whittier Trust's Newport Beach office known for his dedication and accessibility to clients, Batchelor has worked extensively with ultra-high-net-worth individuals and families in San Diego, crafting tailor-made, multi-generational wealth management strategies. His leadership ensures a seamless transition for existing clients while setting the stage for further growth in the region.

"With this new office in San Diego, I am eager to build upon the legacy of trust, integrity and boutique service that Whittier Trust has cultivated for generations," said Batchelor. "I look forward to expanding our connections within the community, enhancing our ability to serve clients locally with tailored financial strategies and contributing to the vibrant culture of San Diego."

Complimenting this milestone of growth, this year also marks the 25th anniversary of Whittier Trust's Seattle Office. The firm also recently opened offices in Menlo Park and West Los Angeles and relocated its headquarters to a larger space in Pasadena to accommodate an increasing number of experienced professionals dedicated to serving a growing client base. As Whittier Trust continues to grow, its focus remains on providing the highest level of personalized service through a relationship-driven, client-first approach.

The office will be located at: 12770 El Camino Real, Ste 120, San Diego, CA 92130, twenty miles north of Downtown San Diego in Del Mar.

For more information about Whittier Trust's wealth management, estate planning and family office services, start a conversation with a Whittier Trust advisor today by visiting our contact page.

From Investments to Family Office to Trustee Services and more, we are your single-source solution.

The momentum from two years of remarkable economic resilience and strong market returns came to an abrupt halt in April 2025. The catalyst for market turmoil this time around was an unexpected turn in the administration’s global trade policy.

April 2, 2025 was touted as Liberation Day in anticipation of the long-awaited details on President Trump’s reciprocal tariff policy. The President used his executive authority to address the lack of reciprocity in U.S. bilateral trade relationships and to “level the playing field for American workers and manufacturers, re-shore American jobs, expand our domestic manufacturing base, and ensure our defense-industrial base is not dependent on foreign adversaries—all leading to stronger economic and national security” (Office of the United States Trade Representative).

However, the scope and magnitude of the proposed tariffs exceeded all expectations. In the initial Liberation Day proposal, all countries were subject to a minimum tariff rate of 10%. Countries with whom the U.S. has a large trade deficit were subject to even higher reciprocal tariffs.

The immediate reaction to the announcement was an immense fear of a global recession and a spike in inflation. Consistent with these fears, stocks sold off dramatically after the initial announcement. A temporary pause in reciprocal tariffs for all countries except China then halted the stock market decline. However, the U.S. dollar and bond market both fell sharply and unexpectedly during the week of April 7, 2025 in contrast to their conventional safe haven status.

We address concerns about higher inflation, higher rates, a recession, a bear market, and a weaker U.S. dollar in this article.

We are aware that this is a highly charged and contentious topic. We will, therefore, refrain from any ideological, philosophical, political, or moral judgment on the subject. We also realize that public disclosures on the topic may lack full transparency for reasons of national security. In a rapidly changing world, our views here have been penned in mid-April 2025.

How Did We Get Here?

The original impetus for higher tariffs is likely rooted in the fact that almost all of our trading partners charge a higher tariff on our exports to them than we do on their exports to us. For example, 2023 World Trade Organization data estimates that China, India and the UK have tariff rates of around 17%, 12% and 5% respectively on U.S. exports to them. In contrast, our corresponding tariffs on their exports to us are around 10%, 2% and 2% respectively. This mismatch in tariffs is probably further exacerbated by other unfair trade practices such as non-tariff barriers and currency manipulation.

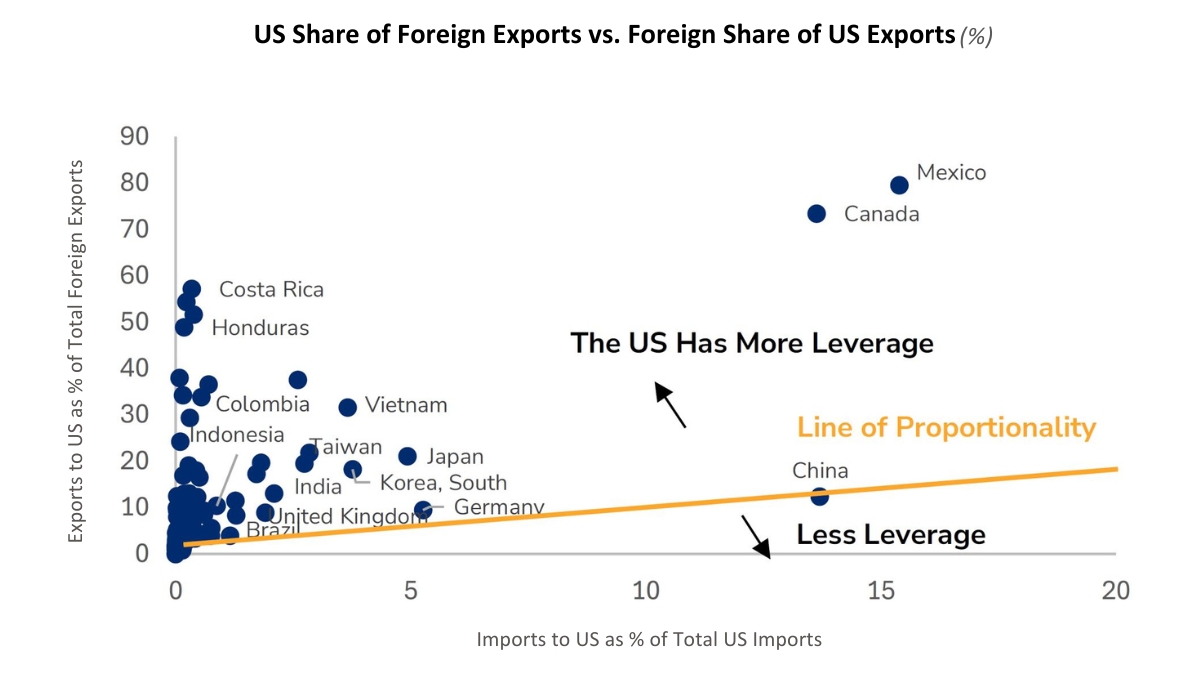

The administration’s policy on tariffs may have been further emboldened by the perceived leverage of the U.S. over many of its trading partners. Figure 1 shows how this leverage is achieved. It compares the importance of a country’s imports to us (x-axis) versus the importance of U.S. exports to its own global trade (y-axis).

Figure 1: Leverage in Trade Relationships

Source: Wolfe Research, World Integrated Trade Solution as of 2022

This chart helps us understand where the U.S. has more leverage with its trading partners. We explain Figure 1 with an example. Take Vietnam for instance. All imports to the U.S. from Vietnam account for only around 4% of total U.S. imports. However, those same Vietnam exports to the U.S. account for almost 32% of its total exports. In light of this imbalance, Vietnam is far more likely to negotiate than retaliate.

In Figure 1, it is clear that Mexico, Canada and several Emerging Markets countries in Asia and South America are most dependent on trade with the U.S., while countries in the EU have more equal trading relationships. China has the most trading leverage against the U.S.; its retaliation has, therefore, been fast and furious.

These salient data points had already been priced into expectations of a higher tariff rate of around 8% prior to Liberation Day. Nonetheless, markets were caught off guard on April 2nd at two levels—by the methodology of tariff calculations and the resulting magnitude of reciprocal tariffs.

Contrary to expectations of a more targeted approach, the reciprocal tariffs were derived from a rudimentary framework that aimed to reduce bilateral trade deficits. Each country’s tariff rate was determined by dividing the U.S. trade deficit with that country by total imports from that country. This number was then cut in half to create the new U.S. “discounted” reciprocal tariff. Here are some of the initial proposed reciprocal tariffs from Liberation Day: China 34%, EU 20%, Japan 24%, India 26%, Vietnam 46%, Switzerland 31% and UK 10%.

These initial reciprocal tariffs have since been suspended for 90 days for all countries except China from April 10th. In sharp contrast, tariffs with China have escalated exponentially through a sequence of retaliations; they now stand at 145% on Chinese exports to the U.S. and 125% on U.S. exports to China. U.S. tariffs on all other countries temporarily stand at the minimum baseline of 10%.

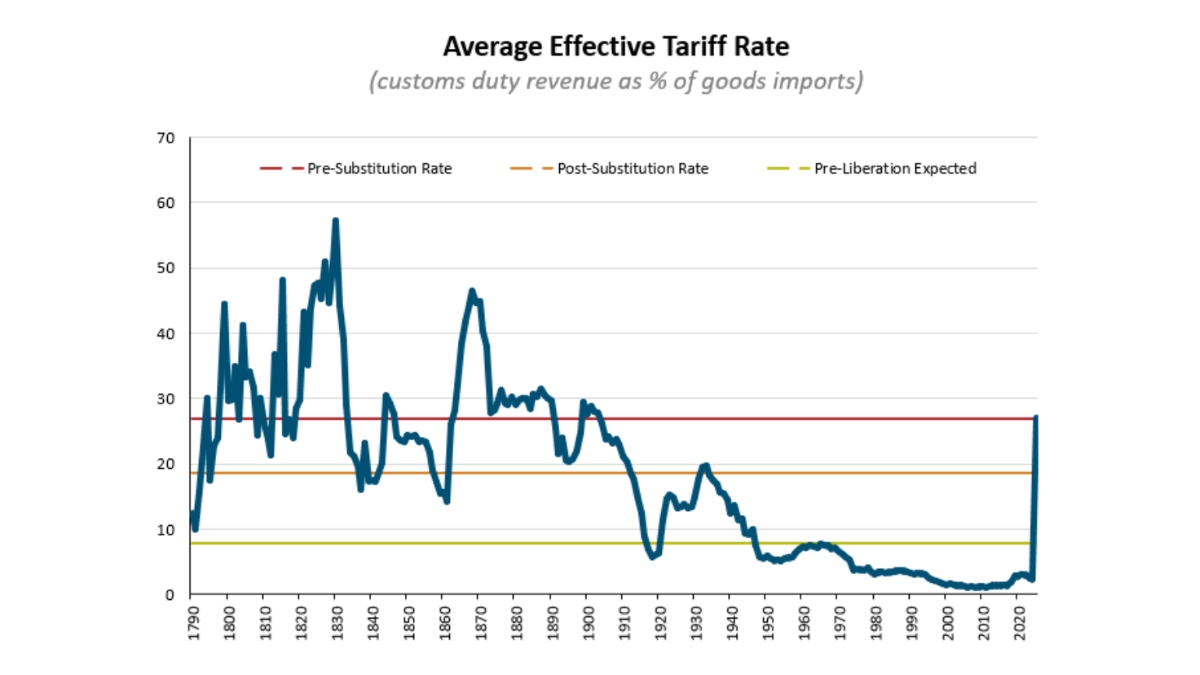

We summarize the revised April 10th levels of tariffs in Figure 2 before turning to our inferences and forecasts.

Figure 2: Average Effective Tariff Rate as of April 10, 2025

Source: The Budget Lab, Yale University

The average global tariff rate for the U.S. is now projected to go up more than 10-fold from 2.4% to approximately 27%. We label this average tariff rate as a “pre substitution” rate since it assumes that all flows of global trade remain constant and intact at 2024 levels. However, higher tariffs on Chinese goods may well trigger substitution to other cheaper imports. The resulting “post substitution” average tariff rate is lower and estimated to be 19%.

Thoughts on Current Trade Policy

We appreciate the desire to increase the U.S. manufacturing base and reduce foreign dependencies in industries critical to national security. We also applaud the pursuit of fairer terms for global trade.

Nonetheless, we initially believed that it was sub-optimal to achieve these goals with an aggressive trade policy alone. A number of tenets in the opening approach seemed misaligned with our global leadership role, created by our own dominant economy and strong alliances with others.

The costs of high fixed trade barriers are well-known, e.g. higher prices, slower growth, less competition, less innovation, and lower standard of living. The expansive and punitive trade war in its initial formulation on April 2nd risked a U.S. recession and an alienation of our allies.

The singular focus on reducing bilateral trade deficits through high imputed tariffs also felt misguided. A large portion of the U.S. trade deficit is driven by principles of comparative advantage where cost of production is often lower overseas and by cultural differences in our lower propensity to save and greater desire to consume. Besides, the large foreign trade surpluses eventually make their way back into U.S. dollar-denominated assets giving our stocks, bonds and currency hegemonic power.

These thoughts may also have preyed on investors’ minds as they indiscriminately sold risk assets. The S&P 500 suffered a 2-day decline of -10.5% on April 3rd and 4th. It was remarkably the first ever decline of such magnitude to be triggered by a policy initiative during benign times – as opposed to an existing endogenous fundamental crisis (e.g. Global Financial Crisis) or an unexpected exogenous shock (e.g. Covid).

Two recent developments have opened up a different possibility for the intent and scope of the current trade war: 1) The U.S. has rapidly escalated tariffs against China all the way up to 145% and 2) The U.S. has rapidly deescalated tariffs on all other countries down to 10% for 90 days. There may now be some credence to a scenario where the trade war is focused on curtailing China’s economic, manufacturing, scientific, technological, and military might while actually strengthening all other global alliances through reconciliation, collaboration and some coercion.

Future Evolution of Trade Policy

We have maintained since the elections that the bark of proposed tariffs will eventually be bigger than its final bite. We have been clearly surprised by the much louder bark and greater magnitude of the new reciprocal tariffs and the damage they have inflicted on the markets so far. Nonetheless, we still believe they will eventually be implemented at lower levels than the ones proposed on April 2nd.

Excluding China, we reckon that global tariffs will settle in at the 8-18% level. While an extensive and protracted global trade war remains a possibility, it is not our base case.

It would serve both the U.S. and China well to find an off ramp towards a more stable co-existence as the world’s two leading economies. If that doesn’t happen for any reason, it is conceivable that the U.S. may largely shift its trade dependence on China to other countries. As supply chains re-adjust, we expect the tariff shock to fade and be subsumed by the positive fundamentals of higher productivity growth, fiscal stimulus and deregulation.

Impact on the Economy

The direct impact of higher tariffs is clearly inflationary and recessionary. We also understand that high levels of policy uncertainty can take an indirect economic toll from reduced consumer spending, slower hiring and lower capital expenditures.

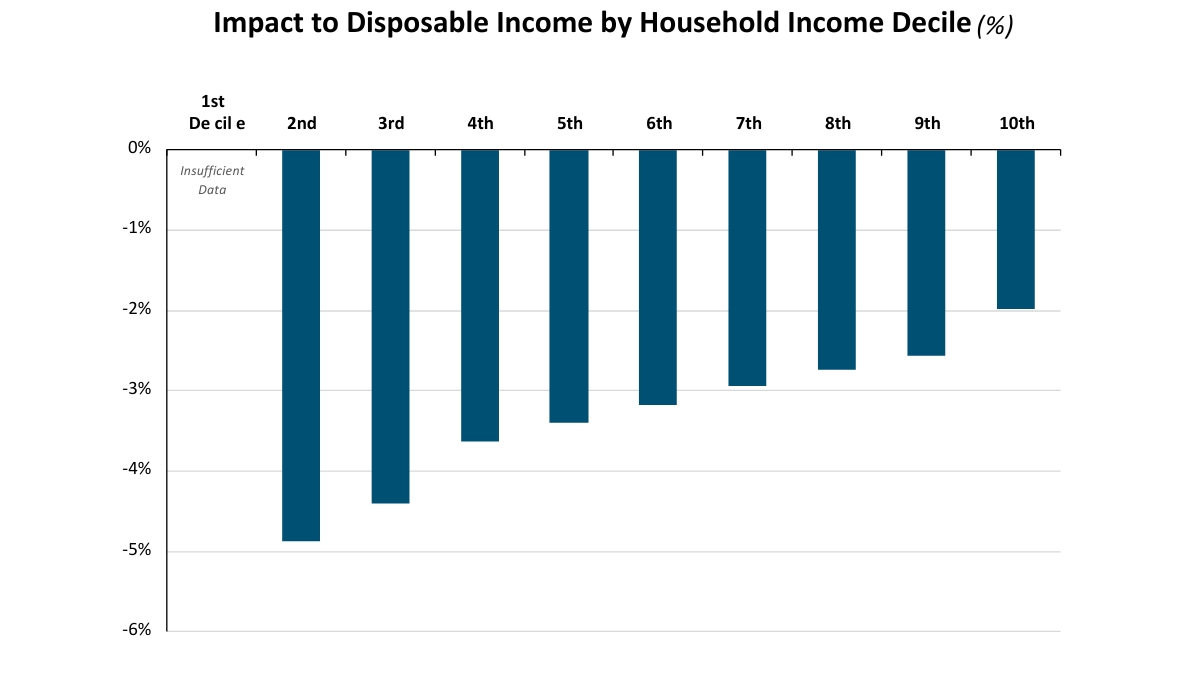

Since higher prices are tantamount to a tax on households, we begin by estimating the impact of tariffs on disposable incomes. Figure 3 shows the likely impact of the April 10 package of tariffs on disposable incomes across different deciles of household incomes.

Figure 3: Impact of Tariffs on Disposable Income

Source: The Budget Lab, Yale University

The top 10% of households by income (highest decile #10) in Figure 3 is expected to see the smallest disposable income decline of -2%. On the other hand, the lowest decile of household income may see disposable income fall by almost -5%.

Any reduction in consumer spending from a decline in disposable income will likely be uneven and disproportionate across income categories. A -2% decline in disposable income for the highest income households may have virtually no effect on their spending. Since most of the aggregate consumer spending takes place in high income households, we are optimistic about a relatively muted impact of tariffs on growth.

We expect up to a -1% direct impact of tariffs on GDP growth and up to a -0.5% indirect impact. Therefore, we expect GDP growth to be reduced by -1% to -1.5% in 2025. From a strong starting point of 2.5% real GDP growth, we expect 2025 growth will still be above zero even after our anticipated reduction.

While the odds of a recession or “stagflation” have gone up, neither scenario is our base case. We estimate the odds of a recession to be 30%, which is well below the consensus expectation of 60-70%.

It is evident that inflation will likely be higher in 2025, but we expect it to subside in 2026 as the world adjusts to a new global trade order. On a positive note, we observe that inflation expectations for a 5-year period starting in 2030 have actually declined from 2.3% to 2.1% as of April 11, 2025. We believe current Treasury bond prices are overestimating long-term inflation risks.

Impact on the Markets

U.S. Stocks

The U.S. stock market has seen some wild swings in 2025. Here is the most striking statistic we have found on recent stock market volatility: If you add up all the absolute intra day moves of 3% or more in the 3 trading days between April 7th and April 9th, the S&P moved a monumental 52%!

In the midst of such high volatility and uncertainty, it is difficult to form an outlook for U.S. stocks. We give the task at hand our best analytical effort and intuitive judgment by forecasting both expected S&P 500 earnings and P/E multiples.

We have observed over the years that earnings growth for the S&P 500 tends to be 3-4 times U.S. GDP growth. Based on our view above that GDP growth may be lower by -1% to -1.5%, we expect S&P 500 earnings growth may also be lower by around -4% to -5%. Despite a reduction in the earnings growth rate because of tariffs, earnings will still rise in the next 12 months.

We have a more differentiated view on where trough multiples will likely end up. In prior recessions, they have fallen to as low as 10-13x. In non-recessionary growth scares, they have fallen to 15-16x.

We believe trough multiples will be higher during this growth scare. The current economic and market crisis is policy-induced; up to a certain point, the antidote for the crisis also remains in the hands of policymakers. And as a beacon of hope and optimism, we already have light at the end of the tariff tunnel in the form of fiscal stimulus and deregulation. Therefore, we strongly believe the trough P/E multiple will be higher this time at about 18x.

We also know that trough earnings and trough P/E multiples are never coincident; you cannot see them simultaneously. You typically see trough prices first, then trough multiples and finally trough earnings.

With these building blocks in hand, we estimate that a viable floor for the S&P 500 may exist at the 4,900-5,000 level. While we obviously cannot rule out lower prices, we may just about avoid a bear market by remaining above its closing price threshold of 4,915.

Our base case rules out a bear market, expects the current correction will not be protracted and predicts the S&P 500 will deliver a positive return in 2025.

U.S. Bonds and Dollar

The manic turmoil in the U.S. bond and currency markets during the week of April 7th could well be the topic of an entire article. We confine ourselves to a few key observations here.

Treasury bond prices and the U.S. dollar both fell significantly in the second week of April. This is an extremely rare occurrence, and it triggered profound fears that we were at the beginning of the end of U.S dominance in global bond and currency markets. Critics attributed the selloff to fundamental factors ranging from heightened U.S. fiscal risks caused by an imminent recession to a devastating loss of confidence in U.S. institutions and leadership.

We do not believe those factors were central to the meltdown in U.S. bonds and the dollar. Instead, we believe it originated from a more nuanced and niche event in the bond market. It is widely understood that hedge funds were unwinding a very large and highly leveraged “bond basis” trade in the face of low liquidity and high volatility. This forced and rapid liquidation created significant price dislocations in both Treasury bonds and the U.S. dollar.

We expect U.S. Treasury bonds and the dollar to stabilize in the coming weeks. We believe the 10-year Treasury yield should be closer to 4.1-4.2% in the near term and around 4.5-4.6% in the long run.

Summary

We close out our discussion on a positive and optimistic note.

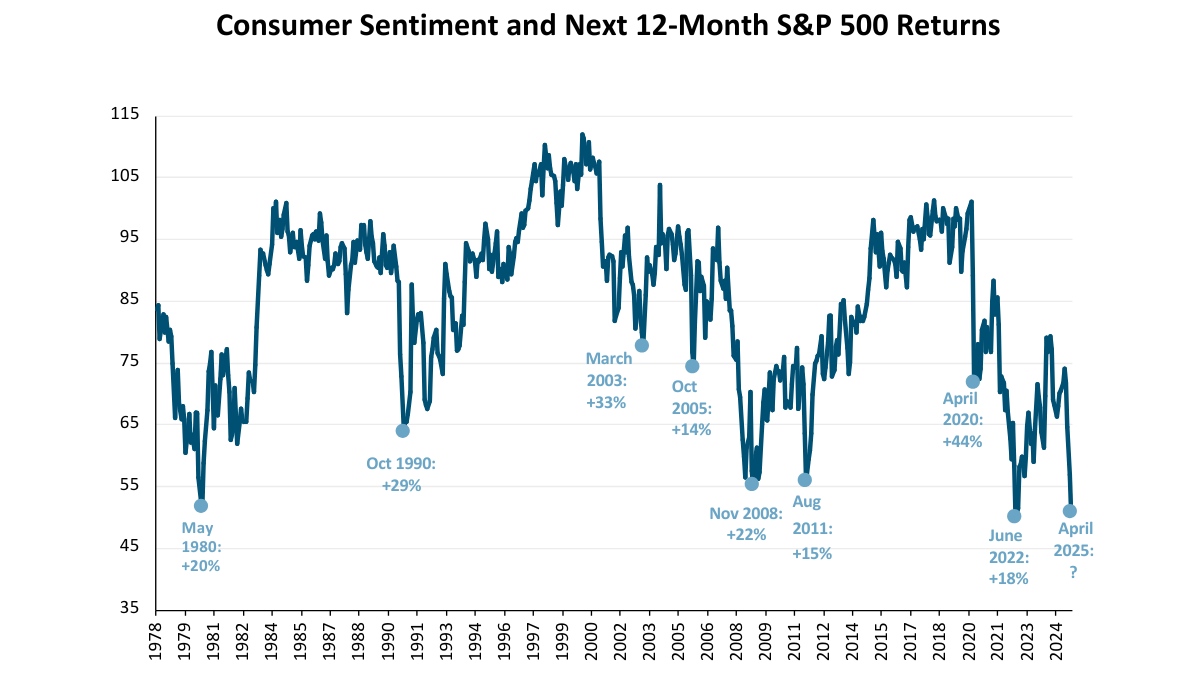

We know from prior experience that high levels of consumer pessimism, policy uncertainty and fear gauges tend to be contrarian in nature. In other words, stock market returns in the aftermath of high pessimism or fear have historically been high. Figure 4 shows the contrarian nature of consumer sentiment.

Figure 4: Consumer Sentiment is Contrarian

Source: University of Michigan, JPMAM, as of April 2025

The latest reading of consumer sentiment nearly reached its all-time low mark of 50.0 on April 11, 2025. While it accurately reflects coincident pain in the economy, it sadly lags the direction of future stock prices.

The stock market tends to look 9-12 months ahead and generally bottoms out when things are at their worst and about to get better. If history is any indication, stock returns over the next 12 months may be handily positive.

We summarize our key takeaways below.

We believe final tariffs will be lower than those proposed currently; their impact on inflation, GDP growth and corporate profits will also be lower than currently feared.

We assign a low probability to a recession, “stagflation” or a bear market.

We do not anticipate a protracted correction in stock prices; we expect the S&P 500 to deliver a positive return in 2025.

We believe fears of “de-dollarization” and significantly higher Treasury yields are overblown; we expect the bond market and the U.S. dollar to halt their declines in the coming weeks.

Within client portfolios, we are focused on adding to or buying new high quality securities that have sold off disproportionately in this “tariff turmoil”. In these uncertain times, we remain careful, prudent, disciplined, and prepared to act on emerging opportunities.

To learn more about our views on the market or to speak with an advisor about our services, visit our Contact Page.

How high-net-worth families can protect their legacy while supporting their heirs.

Every parent dreams that our children will grow up to be happy, productive, contributing members of society. We envision a path that may include youth sports, music and the arts, faith and culture, and of course, education. Our fervent hope is that our efforts to provide the best possible resources to our children will result in highly functioning adults who love us and share our values of family and community. Still, despite the best parenting efforts, highly functioning adults don’t always happen.

Some children come into the world with special needs. Others experience developmental delays or challenges. Still others make it to teen or young adult years relatively unscathed only to experience mental or emotional difficulties, or perhaps even substance abuse, later in life. It is part of the human experience to go through struggles in life and family; financial status is not a guarantee of better outcomes. What is a family to do then, when planning for a multi-generational wealth transfer amid the specter of children (or grandchildren) who are currently incapable of being good stewards of wealth? How does a family plan around a child with severe emotional limitations or addictions?

Where there are obvious physical and developmental difficulties that will require lifetime care and consideration, estate planners frequently suggest “special needs” trusts designed to provide maximum flexibility to support the beneficiary as their needs change throughout life. Far more challenging, however, are situations where alcohol and drug addiction present ongoing issues.

Of course, a family member with substance abuse issues is disruptive on many levels. For parents or grandparents who are planning to transfer assets to younger generations, addiction presents an extra element of complexity. Even if there are not any current issues among family members, we hear from clients all the time that they want to protect their heirs from harm in the event addiction presents itself in the future. Finally, the addict may not be a direct descendent but the spouse or partner of one of our children.

It is well known that irrevocable trusts can be an effective tool in protecting assets from creditors. They are also effective in protecting beneficiaries from their own worst impulses. Since creditors cannot generally reach the assets of the trust, the beneficiary may not use the assets as collateral for a loan. The trustee usually has the power to make distributions on behalf of the beneficiary so funds may be made available for treatment centers and other rehabilitative services. If a family is concerned about the trustee having the power over distributions, they can name a special distribution trustee for this purpose. This allows for professional management and administration of the assets while placing a trusted family member or family friend in the position of making discretionary distribution

decisions.

An alternative (or additional) solution could be to make gifts of limited interests in family entities. For example, a limited partnership interest carries with it an ownership stake but typically no management interest nor the ability to compel distributions. Buy/sell agreements among the partners can help ensure that the ownership stays in the family.

When thinking about how to make funds available for the benefit of a family member with addiction issues, it is important to understand that treatment options are typically quite expensive and insurance may be limited, particularly for residential treatment facilities. Also, it is not unusual for an addict to cycle in and out of treatment and sobriety, requiring multiple stays. Sometimes families will hire a “sober living companion” to live with the individual, and take them to therapy and treatment appointments and even 12-step meetings, if those are part of the recovery plan. The people who provide this service are frequently in recovery themselves and have practical experience navigating different situations. Keep in mind that there is no certifying or accrediting agency to provide credentials for these companions so careful monitoring is appropriate.

The trustee with the power to make distributions for the benefit of the family member will need to take these factors into account when making decisions. It’s not an easy task and there is a high degree of uncertainty. This should be expected, so leniency and flexibility towards the decisions of the trustee should be built into the trust documents. Perhaps the most important job of the distribution trustee is to try and prevent additional harm by making direct distributions to a beneficiary who is under the influence or who is experiencing a particular episode of struggle.

These types of concerns arise in situations outside of clinical addiction. Sometimes it’s not substance abuse but some other kind of distress such as cults or psychologically abusive spouses and partners. In these scenarios, providing a trustee with the discretion to do what they think is in the best interests of the beneficiary is critical. Drafting a trust instrument with highly restrictive provisions, while tempting, may undermine the trustee’s ability to provide resources and care for the intended beneficiary.